Tempted by higher interest rates (like 5.02% from 2 banks) or new account bonuses offered on savings accounts from other banks? Worried about losing (or losing access to) your emergency savings by keeping your eggs in one basket? Inflation may be pinching you at the gas pump and supermarket, but it’s also forcing people to rethink keeping emergency savings in the First Mattress Savings Bank. Now may be a great time to consider additional savings accounts. Here are some reasons and warnings for having multiple savings accounts, along with tips and recommendations for finding the best savings accounts to meet your goals.

Tempted by higher interest rates (like 5.02% from 2 banks) or new account bonuses offered on savings accounts from other banks? Worried about losing (or losing access to) your emergency savings by keeping your eggs in one basket? Inflation may be pinching you at the gas pump and supermarket, but it’s also forcing people to rethink keeping emergency savings in the First Mattress Savings Bank. Now may be a great time to consider additional savings accounts. Here are some reasons and warnings for having multiple savings accounts, along with tips and recommendations for finding the best savings accounts to meet your goals.

Is it worth it?

Rates can vary, but is a higher rate worth the hassle of creating a new account for a few dollars a month? Maybe not, if none of the other reasons below apply. But it’s not just about interest. Account bonuses often come with transaction requirements that may not fit your spending or banking patterns. And what about the hassle of managing multiple accounts, potentially requiring multiple 1099s for tax reporting on the interest earned. Transferring money takes time and can give people headaches. Thankfully, online account creation, ACH transfers and aggregation tools like Empower Personal Dashboard (formerly Personal Capital) and Mint minimize the effort.

Why should I have multiple savings accounts?

You might want multiple savings accounts for several reasons, including interest rate optimization, better access to your emergency funds, simple goal tracking, and reduced risk.

1. Interest Rate Optimization

Recent interest rate increases, bank failures and changes in FDIC withdrawal limits created uncertainty and opportunity for emergency fund savers. Higher interest rates encourage people to moving money in new accounts, many of which offer tiered interest rates where all tiers offer the same high rate. Having multiple accounts allows you to balance your savings portfolio as you would an investment portfolio as interest rates that are changing across accounts and across tiers. If the interest rate drops in one account, you can simply transfer money to a higher-paying account that you’ve already established and linked for ACH transfers.

2. Better Access to Emergency Funds

The “Enhanced Liquidity” offered by multiple accounts allows you to circumvent daily, weekly and monthly limits on deposits and withdrawals. Some banks limit these actions even after the Federal Reserve eliminated “convenient” transfers. Some offer ATM access, which was not considered “convenient” and thus was not previously limited by the Federal Reserve.

3. Simple Goal Tracking

If you are saving for multiple goals like retirement, house or home improvement, car, vacation, wedding, college or instruction accounts for kids, having separate savings accounts for each makes tracking easier. Some accounts support segregating money within a single account, which allows simple goal tracking in a single account.

4. Reduced Risk

Some fortunate people have more than $250K per individual and type of account, the limit for FDIC insurance. Since the limit applies to an individual and type of account at a single institution, you can still protect savings more than $250K by spreading the money across different institutions. But make sure the institutions that hold your money are really different (see below).

Warnings about multiple savings accounts

The benefits may be great, but there are some things to be careful about with multiple savings accounts:

- Total market mutual funds can be a better way to grow money for longer-term goals

- Tiered or minimum amounts for APY reduce interest earned for some savers

- Avoid minimum requirements to get the high APY like:

-

Debit transactions

-

Direct deposit

-

-

New account bonuses are taxable

-

Tiered rates may change

-

Withdrawal limits may change

-

Regulation D suspended transaction limits in 2020 due to COVID, but many accounts still have limits

-

-

Avoid fees:

-

Maintenance fees, sometimes depending on account balance

-

Dormant account fees, which can defeat the purpose of a savings account for emergencies

-

-

Understand FDIC limits

-

Online banks aggregate accounts with parent banks and share the $250K FDIC insurance limit.

- Online banks often use a primary bank’s FDIC protection, so if you have accounts with both, your coverage will be limited to $250K across those accounts. For example, current APY leader UFB Direct states “Bank products and services are offered by Axos Bank®. All deposit accounts through Axos Bank brands are FDIC insured through Axos Bank.“

-

Cash accounts move money to multiple banks to increase FDIC protection. Accounts that circumvent the $250K limit, may or may not tell you which banks have your deposits. This increases the risk of losing your money if you have accounts in the same banks without realizing it.

-

-

Managing multiple accounts requires addition effort for

-

Reconciling / reviewing accounts

-

Filing Taxes (multiple 1099s)

-

Reviewing / storing notifications / statements

-

Using account aggregators like Mint and Empower (formerly Personal Capital), and, soon, Credit Karma

-

Finding the best savings accounts

When comparing high-yield savings accounts at online banks, it’s important to consider these factors:

When comparing high-yield savings accounts at online banks, it’s important to consider these factors:

- Interest

- APY – note the difference between interest rate and Annual Percentage Yield (APY)

- Minimum deposit requirement

- Minimum balance requirement

- Interest basis (simple = principle only, compound = principle + previous interest)

- Compounding frequency (most are compounded and paid monthly based on average daily balance)

- Fees

- Monthly maintenance fee

- ATM fees / reimbursement (domestic / international)

- Dormant account fee

- Other service fees, including excess withdrawal fees

- Access

- Online and mobile banking access

- Daily, weekly and monthly limits on deposits and withdrawals

- ATM access

- Cash deposits

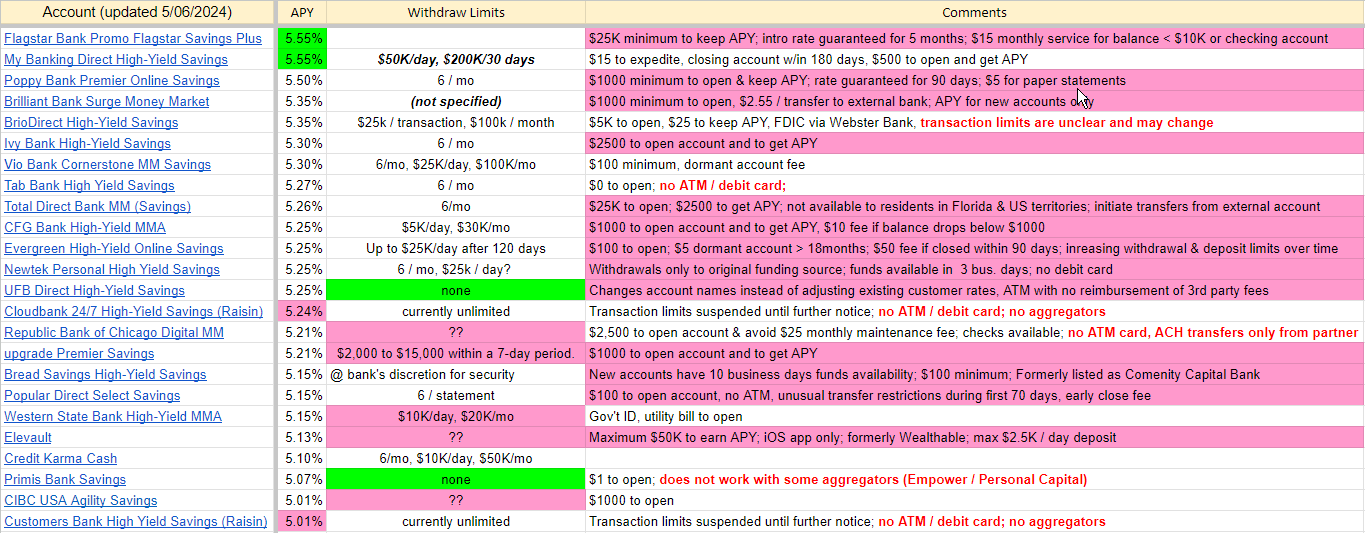

It’s easy to find “best savings accounts” comparisons. Even technology-focused news provider CNET has one. However, most online comparisons and reviews are tied to commissions and may not include all of the best options. For an objective comparison of savings and checking (bill payment) accounts, check out the OPM comparison.

Interest rate optimization is a journey, not a race

Treat savings like any other investment – review your accounts periodically to make sure you’re getting the most out of our cash deposits. The OPM Savings and Checking account comparisons are updated several times each year, depending on market changes. It usually does not make sense to move money from a high paying account to another account that pays slightly higher. But you could move new deposits into a higher paying account.

Optimizing Interest with Multiple Savings Accounts

With a little effort to create accounts and perform periodic reviews, and as long as you are aware of the warnings, you can maximize your savings interest, get better access to emergency funds, track savings goals and diversify your accounts to increase FDIC protection.

{kind=link}

{kind=link}

{kind=link}

{kind=link}